RITC Volatility Trading Platform

Turning options theory into a tested trading system under competition pressure. Built the full solo volatility-case platform for the Rotman International Trading Competition: Black-Scholes pricing, mispricing detection, constrained portfolio optimization, execution, delta hedging, logging, and operational tooling.

Context

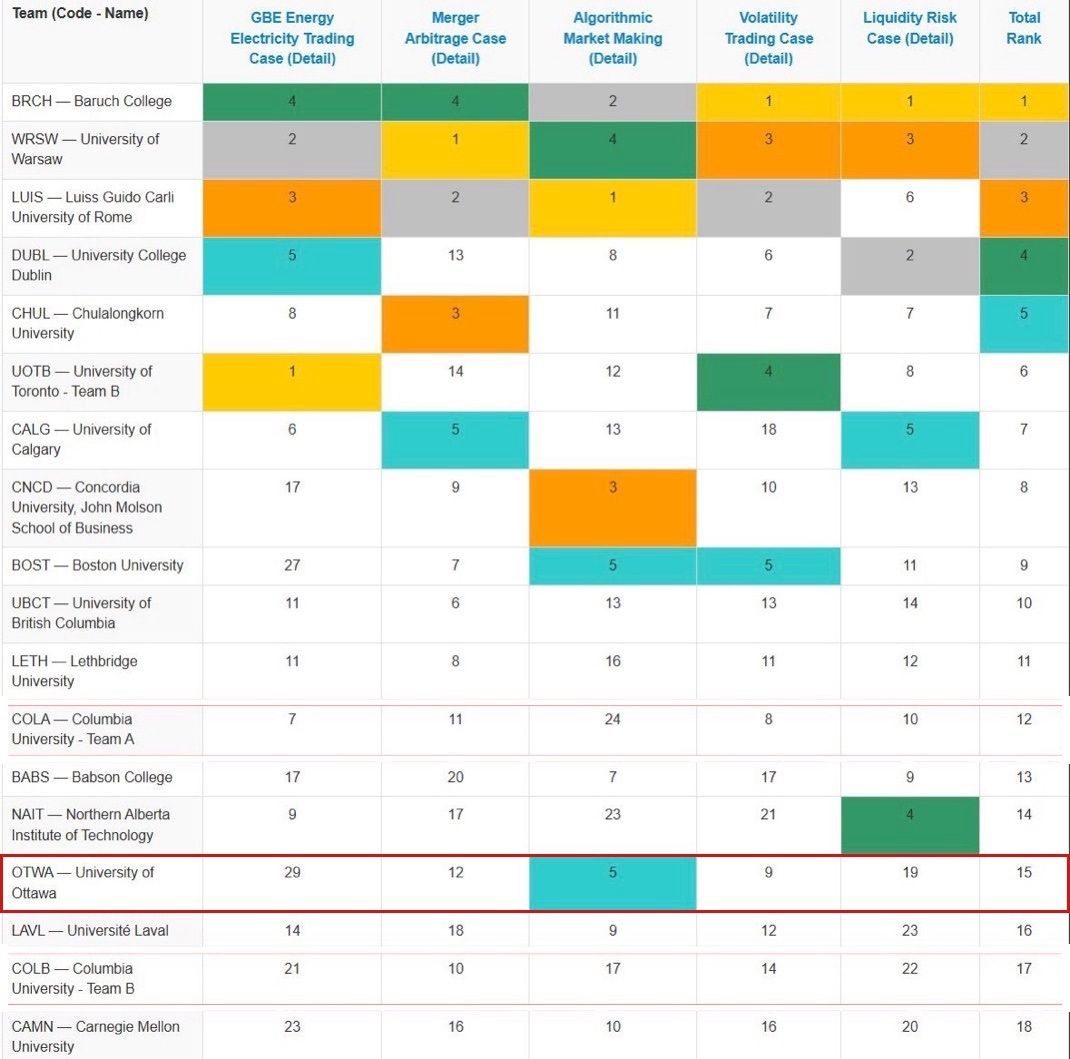

RITC is a three-day global university trading competition built around simulated markets. It was my first trading competition. I represented uOttawa and placed 9th of 38 teams in the solo Volatility Trading case; the team placed 15th of 36 universities overall.

I placed second in the uOttawa team tryout, earned a team spot, and then took full ownership of the volatility case.

The volatility case was the part I owned end-to-end. It was not a market-making strategy. The goal was to understand the case mechanics, identify where options were mispriced relative to theoretical value, and convert that into a repeatable, delta-neutral trading system that could operate under time pressure and strict position limits.

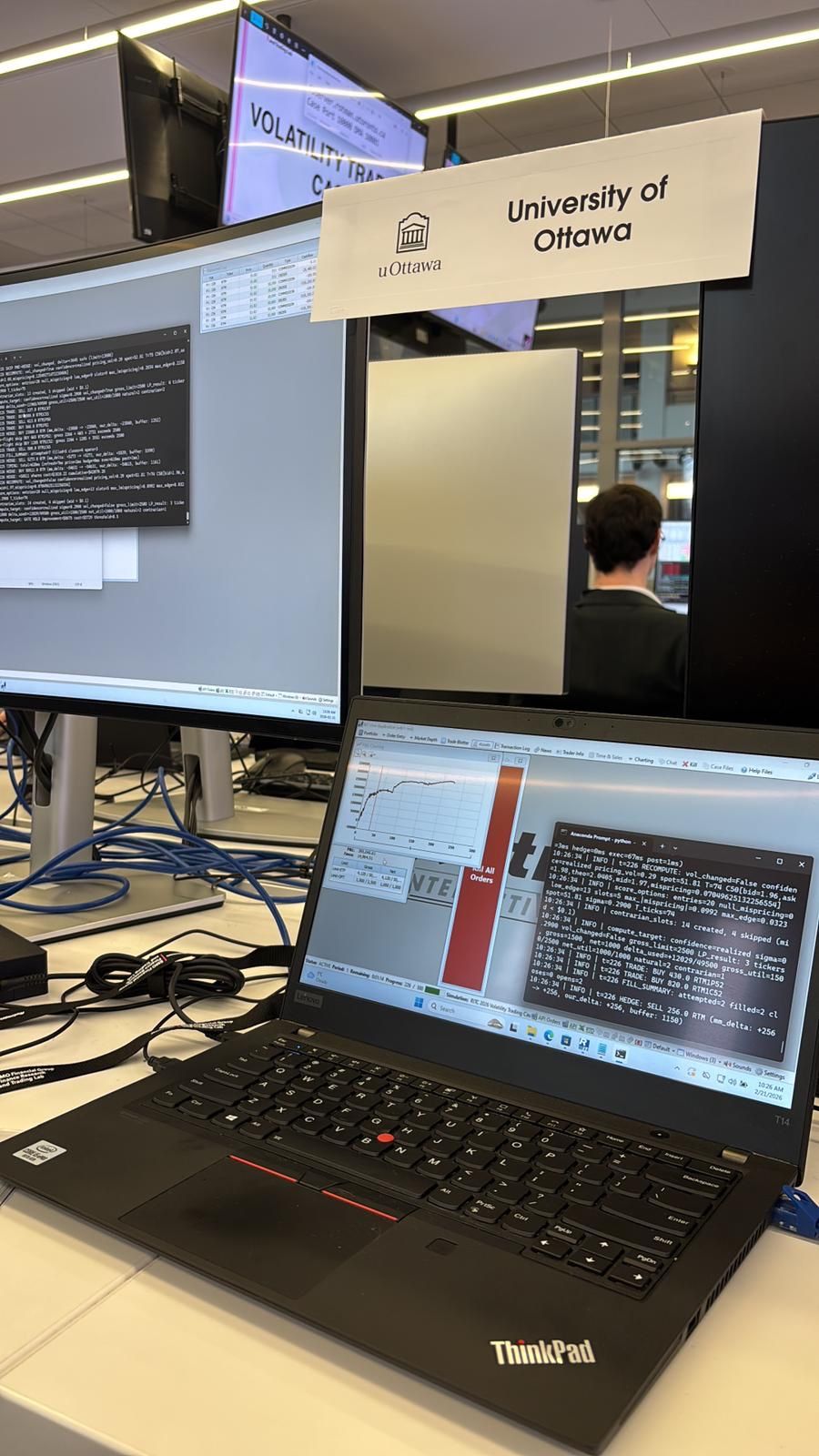

University of Ottawa’s live volatility-case workstation at RITC, with the Python strategy running beside the competition interface.

The harder part was not writing a single pricing script. It was figuring out which options-theory strategy actually produced P&L in the case, then turning that strategy into a system with execution rules, risk controls, logs, and tests.

Problem

The case presented a simple-looking but constraint-heavy trading problem:

- 20 options contracts: 10 calls and 10 puts with strikes from 45 to 54.

- Analyst/news events revealed volatility information over the session.

- Market prices could diverge from Black-Scholes theoretical values.

- Position limits, order-size limits, fees, spreads, delta risk, and time-to-expiry all affected whether a theoretical edge was actually tradeable.

A naive approach would buy anything that looked cheap and sell anything that looked expensive. That was not enough. The system needed to answer a more practical question:

Given the current market, volatility input, option prices, limits, fees, and existing positions, which trades are worth taking now?

My Role & Ownership

What I owned:

- Strategy research for the volatility case

- Black-Scholes pricing and mispricing logic

- Market/news parsing workflow

- Constrained portfolio optimizer

- Execution engine and order sizing

- Delta/risk controls

- SQLite/CSV logging and post-session analysis

- Terminal UI used operationally

Team context: RITC was a broader team competition. The volatility-case platform was my solo build.

System Architecture

RIT REST API + News Feed

↓

Market State Layer

↓

Option Chain + Volatility Parser

↓

Black-Scholes Pricing + Greeks

↓

Mispricing / Edge Calculation

↓

Constrained Portfolio Optimizer

↓

Execution Engine

↓

Delta Hedger + Risk Checks

↓

SQLite / CSV Logs + Post-Session Analysis

↓

Terminal UI for live operationCore Modules

| Module | Responsibility |

|---|---|

api.py |

RIT REST API wrapper for case state, securities, orders, news, trader state |

news_poller.py |

Parsed analyst/news events for volatility forecasts, delta limits, penalty rates |

market.py |

Maintained current market state, positions, Greeks, pricing volatility |

options_pricer.py |

Generated option contracts, priced with Black-Scholes, computed Greeks |

optimizer.py |

Selected trades using scipy.optimize.linprog under constraints |

execution.py |

Traded the diff between current and target positions, close-first |

hedger.py |

Managed RTM delta exposure under penalty and cost constraints |

orchestrator.py |

Composed the live loop: refresh, price, optimize, execute, hedge, log |

Core Trading Logic

The core signal was theoretical-value mispricing:

- Parse volatility/news events for fair-volatility input.

- Price each option with Black-Scholes.

- Compare theoretical value against market bid/mid/ask.

- Buy underpriced options and sell overpriced options, but only when the edge survived fees, spread, position limits, and risk constraints.

- Use linear programming to allocate limited risk and capacity to the highest-value trades.

- Maintain a delta-neutral strategy by hedging the resulting exposure with the underlying when needed.

- Log each session for review and strategy improvement.

Key Engineering Decisions

1. Target-Portfolio Architecture

Instead of sending ad hoc trades, the system computed a desired target portfolio, compared it to current positions, and traded the difference. This made the execution layer easier to reason about and helped avoid churn.

2. Close-First Execution

The execution engine closed positions before opening new ones. That freed gross/net capacity before adding new exposure, reducing failures caused by competition limits.

3. Risk Limits Before Speed

The system included gross, net, delta, per-option, and order-size constraints. In a competition, a fast bad order is worse than a slower valid one.

4. Logging as a Strategy Tool

Every tick/session produced data for later review: market state, option-chain snapshots, trades, volatility events, gamma exposure, P&L attribution, and execution behavior. The logs turned “it felt like the strategy worked” into something inspectable and improvable.

5. Operational Interface Matched the Real Need

A React/TypeScript/Tailwind dashboard was built during development, but the live competition workflow ultimately did not need a heavy web dashboard. The operational interface moved to a faster terminal UI. A useful lesson: the best interface is the one that fits the task, not the one that looks best in a demo.

Result

Published RITC results with the University of Ottawa row highlighted: 9th in Volatility Trading and 15th overall.

View my original LinkedIn competition recap.

Accuracy Notes

- This was not market making.

- I did not win RITC; the team placed 15th.

- The volatility case was built solo; broader RITC was a team event.